- Admissions

- Academics

- Research Office

- Student Life

- News & Events

- Outreach

- About

Dr. Consigli was born in Rome on June 28, 1959. He is married with one son.

He graduated in Economics with honour at University La Sapienza of Rome in a.y. 1982/3 and then specialised in Banking and Finance with a Master in June 1990 prior to his PhD in Mathematics completed at the University of Essex in 1995. Throughout, from 1986 to 1992 he was full time employee of a Finance company in Rome.

Dr. Consigli between 1995 and 1997 was PostDoc at the University of Cambridge (UK) and member of Center of Financial Research within the Judge Institute of Management Studies directed by Professor M.A.H. Dempster.

In 1998 he returned to Italy and worked for 4 years as Vice president at the Directorate of UniCredit Italiano and then as reposnsible of quant developments in the investment bank Unicredit Banca Mobiliare.

Between 2003 and 2004, he started an individual career as Consultant for advanced risk management and quantitative financial tool developments for the financial and insurance industry and during this period in 2004, he won a National competition with the Italian Ministry of University to become Associate Professor. The year after he joined the University of Bergamo and continued his activity as consultant and industry advisor as member of the Dept of Mathematics through external R&D grants with the private sector. In 2014 (2012 cohort) he won the first National competition to become eligible for Full professorship in Applied mathematics for social sciences under the Italian jurisdiction.

Between 2015 and 2017, dr Consigli has been appointed as Strategic advisor for internal developments by the Headquarter of the Allianz S.A. insurance conglomerate. A position compatible with his full time academic role.

FSU-2022-010, 6238. Title: Machine Learning and Optimization approaches for dynamic control problems in finance, July 2022-June 2024.

Machine learning (ML) methods have shown in recent years their potential in several areas of financial practice and research, primarily related to the solution of asset pricing problems, market forecasting and related portfolio selection problems. The latter mainly within static, one-period problems. In a dynamic setting specific statistical learning (SL) techniques have been applied to-date to Markov decision problems (MDP) relying on stochastic dynamic programming (SDP) to find good value or policy functions’ approximations under model-based approximate dynamic programming (ADP) or model-free reinforcement learning (RL). This project focusses on the extension of ML and SL techniques to dynamic financial problems under uncertainty. This field is at the crossroad of three major research areas: (a) stochastic optimization, (b) finance and (c) statistical learning. The primary aim of the project is then be associated with the validation of emerging ML-based methods and optimization approaches within a unified methodological framework. Such framework is applied to a sufficiently general class of decision problems under risk, namely investment-consumption problems formulated however under a pair of novel decision rules. Specifically related to continuous stochastic dominance (SD) orderings and based on assets’ risk marginal contributions as driving portfolio diversification principle.

GBS-pALM project (2022-2023): The University For Innovation (U4I) Foundation funds R&D projects aimed at producing a highly innovative, patent-based tools with potentially relevant market impact. It is a highly competitive funding resource available to academic institutions and research centers in Italy. The project acronym stands for Goal-based sustainable personal asset-liability management.

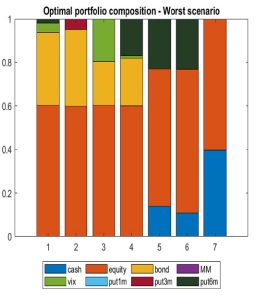

The ultimate beneficiaries of pALM are retail investors, individuals or households whose financial planning projects may develop from medium (such as house purchase and children’s education) to long-term horizons (such as pension savings) and are assumed to be characterized by goals or targets. Specific to this project is the definition of a dynamic policy able to maximize individuals’ welfare through a combined goals-achievement and protection strategy while considering individual and family constraints as required by modern regulatory requirements (e.g. Mifid). The definition of investment opportunities in the class of environmental, social and corporate governance (ESG) compliant investments is also a specific feature of this proposal. Those are then to be considered the key R&D areas on which this project builds: (a) optimal individual investment-consumption planning, (b) environmental and financial sustainability, (c) long-term decision support, (d) goal-based investing with retirement targets and (e) machine learning techniques. The result of the project will be a web-based system coded in open-source programming language that merges a goal-based and long-term dynamic decision tool, with the state-of-the art of machine learning for a large class of retail investors.

DRO-LDI project in cooperation with GeorgiaTech (US) and University of Milan Bicocca (IT) (2019-2023): Distributionally robust liability driven investment for occupational pension funds.

This reseach project follows a long term cooperation with the ISyE institute at GeorgiaTech devoted to stochastic optimization methods and applixations. We consider here a second pillar defined benefit (DB) occupational pension fund (PF) asset-liability management (ALM) problem from the perspective of a PF manager delegated to pay benefits to the employees – the PF members – by a company – the sponsor – who is also funding the pension plans. The pension fund collects the contributions from the sponsor and pays the benefits to the passive members. We do not consider the possibility to cover the fund through an insurance company (which in certain systems is compulsory). The PF manager objective is to determine an investment strategy that allows the fund to cover its liabilities while minimizing the cost of funding, given by the contributions payed by the sponsor and the deficit between liabilities and total asset value at the end of the time horizon. We take into account uncertainty over members’ lifetime and assets returns. In particular the Lee-Carter model is considered for the survival probabilities and the Nelson/Siegel one for the yield curve. The ALM problem is formulated in constant monetary values to immunize the impact of inflation. To solve the problem we propose a distributionally robust stochastic optimization (DRSO) approach and analyze how the choice of metric affects the worst-case distribution and the out-of-sample performance of the solution.

This is the last research work of a series of projects all focussing in pension funds quantitative ALM problems, a long term research interest of dr Consigli with publications in primary Journals since his highly cited 1998 article with M.A.H.Dempster on Dynamic Stochastic Programming for Asset Liability Management (see the Google Scholar page)

Dynamic portfolio management, volatility trading, risk control, stochastic dominance (2018-2022)

This is a research stream that I carry on with academic colleagues based on my interest on dynamic investment theory in a discrete setting and optimal risk control based on market signals and derivative contracts. I have two research article recently published in Q1 journals with a colleague from Univ. Ca’ Foscari of Venice and with the colleagues from Jiaotong university. In the first article we extend a canonical multistage dynamic model to include complex derivatives portfolios and strategies. In the other article, which is ambitious we are proposing a new stochastic dominance criterion which is applied to portfolio selection. Finally with the same colleagues from Jiaotong university we have recently published a paper on dynamic risk control under stochastic volatility and a mixture of copula functions aimed at improving tail control in periods of financial instability.

DAPO for P&C ALM v 1.0, v 2.0, v 3.0 and v.4.0 (2010-2019) R&D project funded by Allianz Investment Management (AIM) Italy and Munich (HDQ) Allianz Group, on Property and Casualty Asset-Liability Management. Dr Consigli was Coordinator and Project leader of the UniBG team. (phase 1: October 2010-September 2011; phase 2: October 2011-March 2012; phase 3: July 2012-December 2012) and for 4.0 (July 2018-January 2019) Dr Sebastiano Vitali and Dr Vivek Varun . Key project features: pilot system for long term (10 years) P&C ALM based on stochastic programming techniques, core and alternative investments. Multi-criteria objective function with functional and regulatory constraints, global problem. Software environment: Matlab with Excel I/O and GAMS model generator and solution methods. is.

My ORCID: orcid.org/0000-0002-7718-347X

Recent publications:

J1. G.Consigli, J.Liu and J.P.Zubelli (2024): Optimal dynamic fixed-mix portfolios based on reinforcement learning with second order stochastic dominance. Online first on Engineering Applications of Artificial Intelligence (Elsevier), 1-35.

J2. A.Gomez, G.Consigli and J.Liu (2024): Multi-period portfolio selection with interval-based Conditional Value-at-Risk. In print on Annals of Operations Research (2024), 1—38

J3. J.Liu, Z.Chen and G.Consigli (2023): The cost of delay as risk measure in target-based multi-period portfolio selection models, IMA J of Management Mathematics, OUP, online, 1—32

B1. G.Consigli (2023): Financial Regulation and Risk Measures. Volume In the footsteps of Giorgio Philip Szego. Castellano, D’Ecclesia and Zambruno Eds, Int.l Series on Operations Research and Management Science (Springer, U.S.), 21—28

J4. B.Ji, Z.Chen, G.Consigli and Z.Yan (2022): Optimal long-term Tier 1 employee pension management with an application to Chinese urban areas. Quantitative Finance 22 (9) (Taylor & Francis), 1759-1784, https://doi.org/10.1080/14697688.2022.2092329

J5. D.Lauria, G.Consigli, F.Maggioni (2022): Optimal chance-constrained pension fund management through dynamic stochastic control. OR Spectrum (Springer), Online Mar2022, 1—42, doi: 10.1007/s00291-022-00673-0, Open access.

J6. D.Barro, G.Consigli and V.Varun (2022): A stochastic programming model for dynamic portfolio management with financial derivatives. Journal of Banking & Finance 140, 1—21 doi: https://doi.org/10.1016/j.jbankfin.2022.106445 Open access.

J7. G.Consigli, M.Kopa and A.Pichler (2022): Discrete stochastic optimization in finance. S.I. ICSP2019 conference, Quantitative Finance (22:1), 28--30, DOI: 10.1080/14697688.2021.2013621

J8. J. Liu, Z. Chen and G.Consigli (2021): Interval-based stochastic dominance: theoretical framework and application to portfolio choices. Annals of Operations Research, 307(1), pp.329-361, https://doi.org/10.1007/s10479-021-04231-9

Dr. Consigli curriculum develops over the years with a strong commitment to research in applied mathematics and a relevant stream of cooperations and projects with the financial and insurance sectors. As witnessed in the biography he spent rougly a decade as employee in the finance sector, four years as a consultant and almost two decades in academia. Dr Consigli research interest are in the areas of financial modelling, optimization methods, stochastic analysis and increasingly over the years computational and numerical methods. dr Consigli has a rich editorial experience primarily devoted to Stochastic optimization methods in economics, finance and energy resulting to date (2022) in 10 special issues with Q1 journals. He is Area Editor of the IMA J of Management Mathematics (O.U.P.), OR Spectrum (Springer) and AE of Computational Management Science (Springer) and the International J of Risk Management and Financial Engineering (InderScience). As editor and author of three volumes of the Springer Series on Operations Research and Management Science (2011,2016, 2018) he qualifies as Springer author.

Dr Consigli organized and was scrientific chair of several International conferences through the years and coordinated 2 postgraduate international training programs in Stochastic Optimization methods with applications (2007-2009, 5 universities involved: UniBG, University of Vienna, University of Edinburgh, Brunel University of London, Norwegian University of Science and Technology (NTNU) and in Computational Management and Application (2015-2017, bilateral cooperation with ISyE, GeorgiaTech, Atlanta).

He is member of the following scientific associations and societies (in alphabetical order):- a) Bachelier Finance Society (BFS) www.bachelierfinance.org , b) Euro Working Groups on Commodities and Financial Modelling (EWGCFM) https://www.euro-online.org/web/ewg/8/ewg-cfm-euro-working-group-on-commodities-and-financial-modelling, and Stochastic Optimization (EWGSO) https://www.euro-online.org/web/ewg/35/euro-working-group-on-stochastic-optimization c) Fellow of the Institute of Mathematics and Applications (FIMA, UK), d) Italian Associations of Applied Mathematics for Social Sciences (AMASES) https://www.amases.org and Operations Research (AIRO) https://www.airo.org , e) Stochastic Programming Society (SPS, Technical Section of the Mathematical Optimization Society) https://www.cosp.org.

During the last 5 years, he has been invited or Keynote speaker in the following conferences:

16-17.9.2023: Bandung (Indonesia) ICOFM2023 International Conference on Optimization and Financial Mathematics organized by Institute of Technology of Bandung. Keynote speaker: SD principles enforced through interval-CV@R in dynamic mean-risk portfolios. https://math.itb.ac.id/icofm-2023/

24-28.7.2023: Davis (USA) ICSP2023 XVI International Conference on Stochastic Programming, invited semiplenary speaker in the Mini Symposium on Advances of Stochastic Dominance: theory and applications. Semiplenary: Stochastic dominance principles applied to optimal financial planning. https://na.eventscloud.com/website/40825/home/

12-16.4.2023: Cambridge (UK) University of Cambridge Quantitative Finance conference, Clare College. Keynote Speaker: MAH Dempster’s major contributions to stochastic optimization and finance and talk on Benchmarking Pension Fund management methods.

29.6-1.7.2022: Venice (IT) ECSO-CMS2022 International European Conference on Stochastic Optimization and Computational Management Science. Invited plenary speaker https://www.unive.it/pag/38159.

21-24/11/2021: Research in Options 2021, Khalifa Univ, Bloomberg and Univ.Fed.S.Caterina (Brasil). Invited speaker: Optimal option portfolios with volatility as asset class in a discrete market.

29.9.2019: Trondheim (NO) ICSP2019 XV International Conference on Stochastic Programming, https://www.ntnu.edu/web/icsp/icsp2019 , invited semiplenary speaker in the Mini Symposium on New frontiers in finance. Semiplenary: Asset-liability management under distributional uncertainty: benchmarking SP-based optimal policies with DRO.

26-28/11/2018: Buzios (Brasil) Research in Options 2018, https://impa.br/en_US/eventos-do-impa/eventos-2018/research-in-options-2018/ organized by IMPA. Invited speaker: Derivatives-based portfolio management via multistage stochastic programming.

12-13/4/2018: Seoul (South Korea) 4University rotating Fintech conference, 2nd conference held in Seoul and organized by KAIST http://wmt.kaist.ac.kr/eng/conference.html. Invited plenary: Asset-liability management and goal-based investing for the Retail business in the robo-advisory era.

Plus attending regularly International conferences in Optimization, Applied Mathematics, Operations Research, Computational Management Sciences and Stochastic Programming.